Avanath advances, building large new investment fund, buying City Point tower after 535 Carlton & 38 Sixth; are more Brooklyn investments coming?

Avanath Capital, the California-based privately-owned firm that bought the "100% affordable" 535 Carlton and 38 Sixth--oddly dubbing them (for a while) "Barclays I" and "Barclays II," erroneously (for a while) identifying the location as "Pacific Heights," and dubiously claiming that some units were "market-rate"--is in expansion mode nationally.

That includes Brooklyn, as Avanath recently bought 7 DeKalb, a building that's part of the City Point complex in Downtown Brooklyn.

That's thanks to new investments by pension funds and others interested in remunerative ESG (Environmental, Social and Governance) investing, which encompasses "affordable housing." That's no small irony, given that the income-targeted, below-market housing in Atlantic Yards/Pacific Park is, in the main, not very affordable.

“This latest acquisition, combined with our recent purchase of two apartment communities adjacent to Barclays Center"--not quite; only one is--"and approximately a half-mile from 7 DeKalb, brings Avanath’s total footprint in Brooklyn to 852 units,” Avanath's Williams said in the article, suggesting "the assets will benefit from operational efficiencies enhanced through economies of scale, which could further contribute to future cost savings and investment upside.”

Avanath's Keith Harris, Executive Vice President of Acquisitions, said "the firm continues to be drawn to high-quality assets in Brooklyn."

More on the new fund

In a 3/22/22 announcement, Avanath Announces Initial Closing of Open-Ended Affordable Housing Fund, Avanath said it had $536 million in equity commitments, allowing it to acquire an $830 million affordable housing portfolio--27 apartment communities--and to provide cash for additional acquisitions.

Unlike other funds, apparently with a limited term, "the Fund’s infinite lifespan enables us to invest on an ongoing basis in affordable housing," Carter said.

“With the establishment of the Fund, our team will be able to continue our focus on markets that exhibit high income growth, high housing costs, and a significant supply-demand imbalance,” stated Avanath's Wesley Wilson. That certainly could include Brooklyn.

“Typically, properties in which this Fund invests will have enjoyed a 95%+ occupancy rate with significant waitlists," Wilson said. "The tenancy of our portfolio has a median length of 6 years versus approximately 1+ years for market-rate properties, which positions these assets for stability.”

In a 1/26/23 announcement, Avanath Announces Close of Over $205 Million in Additional Equity Commitments for Open-Ended Fund, the firm's John Williams noted that, since the initial closing, they'd "purchased four additional communities with equity from the Renaissance Fund,” and were able to resist the industry's stall.

Avanath's approach

That's thanks to new investments by pension funds and others interested in remunerative ESG (Environmental, Social and Governance) investing, which encompasses "affordable housing." That's no small irony, given that the income-targeted, below-market housing in Atlantic Yards/Pacific Park is, in the main, not very affordable.

Avanath, according to PERE News, a publication specializing in the private real-estate market, "is one of the few private real estate managers owned and led by a Black executive." It had $2.8 billon of assets under management" as of that 3/17/22 article.

The new Avanath Affordable Housing Renaissance Fund got $50 million from Michigan's pension fund, according to a 3/17/13 article from IPE Real Assets, which noted that the fund "targets a 10% to 11% net internal rate of return with an annualized distribution yield of 4% to 5%." It had targeted targets returns "in the low-to-mid teens" for its previous funds, according to PERE News.

More in Brooklyn?

So it's not implausible that Avanath, with its foothold in Brooklyn, might consider a further role in Atlantic Yards/Pacific Park. While it's mainly an operator of housing, it does have some ambitions for ground-up investments.

Founder/Chairman/CEO Daryl Carter, writing in the company's Winter 2022 newsletter (also at bottom) upon the closing of Avanath's first open-ended affordable housing fund, the Renaissance Fund, noted that " institutional investors – particularly those with more socially-conscious decision makers at the helm – have been increasing allocations to affordable housing to meet their ESG goals."

"This closing represents our ability to accelerate Avanath’s growth and widen our acquisition capacity as we continually invest in affordable housing that builds communities and improves lives for those in need across the nation," he wrote, adding that they'd "be selectively pursuing a limited number of new, ground-up development initiatives to add to the supply of affordable and workforce housing."

Note the use of the term "workforce housing," which was used, at least early on in the Atlantic Yards saga, for the middle-income, below-market units. That was before the term "affordable"--technically, units targeted to 30% of income--began to subsume all those units.

Avanath held its 2022 meeting last December at 1 Hotel Brooklyn Bridge, at the waterfront in Fulton Ferry/DUMBO, within Brooklyn Bridge Park.

Another Brooklyn transaction

Real Estate Weekly, surely drawing on a press release, on 1/22/23 published Avanath Capital Management Acquires High-Rise Apartment Community in Brooklyn for $101.25 Million:

Real Estate Weekly, surely drawing on a press release, on 1/22/23 published Avanath Capital Management Acquires High-Rise Apartment Community in Brooklyn for $101.25 Million:

The acquisition of the 18-story high-rise community, purchased with equity from Avanath’s Renaissance Fund, is aligned with the firm’s mission to develop, own, and operate communities in growing submarkets that provide quality housing to residents of all income levels...7 DeKalb includes 250 units, with 200 of them below-market: 150 middle-income units at 130% of Area Median Income (AMI), 8 low-income at 40% of AMI, and 42 low-income at 50% of AMI. See below.

Note that Avanath officially targets lower-income households as well as "workforce housing" serving households earning 80% to 120% of AMI. So 60% of the units at 7 DeKalb are for households at 130% of AMI, while 50% at 535 Carlton/38 Sixth are aimed at those earning 165% of AMI, with another 15% are aimed at those earning 145% of AMI.

“This latest acquisition, combined with our recent purchase of two apartment communities adjacent to Barclays Center"--not quite; only one is--"and approximately a half-mile from 7 DeKalb, brings Avanath’s total footprint in Brooklyn to 852 units,” Avanath's Williams said in the article, suggesting "the assets will benefit from operational efficiencies enhanced through economies of scale, which could further contribute to future cost savings and investment upside.”

Avanath's Keith Harris, Executive Vice President of Acquisitions, said "the firm continues to be drawn to high-quality assets in Brooklyn."

"The asset was acquired off-market from the seller, The Brodsky Organization," according to the article. The purchase price, according to The Real Deal, was "only slightly above the $100 million that Brodsky paid in 2017," buying it from developers Acadia Realty Trust, Washington Square Partners and BFC Partners.

Another connection

Note that Brodsky, which invested in Atlantic Yards/Pacific Park by buying rights to the B15 parcel (662 Pacific St., aka Plank Road) and then partnering with master developer Greenland Forest City Partners on B4 (18 Sixth Ave., aka Brooklyn Crossing), then in February hired Scott Solish, Greenland USA's Atlantic Yards/Pacific Park point man. (Greenland USA owns nearly all of the joint venture.)

Solish separately intersected with Avanath when the joint venture sold that firm the two "100% affordable" 535 Carlton and 38 Sixth. So Brodsky and Avanath, perhaps, have an ongoing connection.

Rising rents?

One of the few ways to get more money--compared to ongoing projections--from rent-regulated housing may be to lift rents to their legal limits, and that may have been Brodsky's strategy.

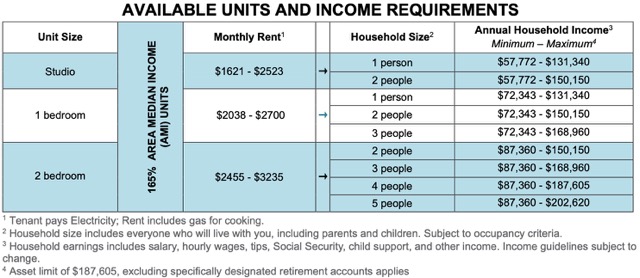

Note that, in 2020, when Brodsky was re-marketing the middle-income units (see below), the rents were listed as ranges:

- Studio: $1621 - $2523

- 1-BR: $2038 - $2700

- 2-BR: $2455 - $3235

That doesn't quite compute. Note that the lower rent levels in the range refer to the rents when the building launched, while, as of 2020, rent levels at 130% of AMI, were: studio: $2,155; 1-BR: $2,700; 2-BR: $3,235.

Those guidelines can be exceeded, so it's possible that Brodsky was able to lift the rent, and/or was projecting future increases.

(Avanath recently advertised an Open House for 535 Carlton, surely the middle-income units, so it's worth watching to see whether/how they try to maximize rents.)

At 7 DeKalb, according to StreetEasy, the most recent market-rate 1-BRs have ranged between $3,371 and $4,031, and the 2-BRs have ranged between $4,787 and $6,560.

Rising garage revenues?

In March 2019, Bisnow reported on Avanath's purchase of an apartment complex in Chicago, quoting a broker as saying, “In addition to the buyer’s focus on affordable housing, they saw opportunities to add value in the market-rate units and the parking garage as well."

Could that mean an effort to drive more revenue from the parking garage--under expansion from 303 spaces to 758 spaces--under 535 Carlton?

In a 3/22/22 announcement, Avanath Announces Initial Closing of Open-Ended Affordable Housing Fund, Avanath said it had $536 million in equity commitments, allowing it to acquire an $830 million affordable housing portfolio--27 apartment communities--and to provide cash for additional acquisitions.

Unlike other funds, apparently with a limited term, "the Fund’s infinite lifespan enables us to invest on an ongoing basis in affordable housing," Carter said.

“With the establishment of the Fund, our team will be able to continue our focus on markets that exhibit high income growth, high housing costs, and a significant supply-demand imbalance,” stated Avanath's Wesley Wilson. That certainly could include Brooklyn.

“Typically, properties in which this Fund invests will have enjoyed a 95%+ occupancy rate with significant waitlists," Wilson said. "The tenancy of our portfolio has a median length of 6 years versus approximately 1+ years for market-rate properties, which positions these assets for stability.”

In a 1/26/23 announcement, Avanath Announces Close of Over $205 Million in Additional Equity Commitments for Open-Ended Fund, the firm's John Williams noted that, since the initial closing, they'd "purchased four additional communities with equity from the Renaissance Fund,” and were able to resist the industry's stall.

"The Fund’s portfolio currently includes 27 properties totaling 4,786 units and is valued at nearly $1.2 billion with more than $750 million of equity commitments from more than 15 institutional investors," the press release stated.

Avanath's approach

Carter stated in the newsletter, "As ESG becomes increasingly important to the world at large, capital flows to social programs will continue to rise – especially programs that serve to elevate the lives of affordable housing residents in a multitude of ways."

Carter, testifying 4/30/19 before the House Committee on Financial Services on behalf of the National Multifamily Housing Council and the National Apartment Association, stated:

Families with incomes of $30,000 to $80,000 represent the largest segment of the rental housing market.

That's consistent with Avanath's stated investment strategy. Note that a majority of the income-targeted units at 535 Carlton and 38 Sixth have incomes well above that, but, of course, New York is a more expensive city than most. Carter continued:

We regard the ability to serve this market as a social, cultural and financial opportunity, so we invest not only in brick and mortar, but in on-site services, amenities and activities that add value to properties and bring our residents’ desired lifestyles within reach. Some of our onsite efforts include after school programs for young people, financial literacy seminars, and wellness activities for seniors.

Let's see if/when that happens in Brooklyn.

There's a business logic, as well:

Avanath believes that the affordable housing sector provides excellent and sustainable riskadjusted returns with high barriers to entry and strong downside protection.Policy recommendations

Carter spoke on behalf of the industry:

As policymakers consider infrastructure initiatives, we urge the inclusion of measures to support housing including those that would:

• Ensure a long-term and stable transportation funding stream to provide state and local governments, and the private sector, with the certainty and resources they need to meet their infrastructure needs and make further infrastructure investments;

• Encourage and incentivize all levels of government to remove barriers to apartment development and streamline regulatory burdens;

• Invest in rehabilitating existing communities;

• Address the challenges of housing affordability and stimulate new affordable development through density bonuses, fast-track review and by-right development; and

• Upgrade municipal infrastructure to accommodate growth and facilitate remediation of safety and environmental hazards that burden housing and new construction.

Comments

Post a Comment