Shanghai-based Greenland Holdings, credit rating plummeting, slides closer to default; subsidiary's claim of commitment to Pacific Park requires more evidence

The news looks ominous, as The Real Deal summarized it yesterday, Default risk for Chinese parent of Pacific Park developer, a Shanghai-based conglomerate damaged by ambitious development plans and COVID lockdowns (though the latter has just eased).

|

| Screenshot from Google Finance |

That led to two, multi-notch downgrades in a week from the two main credit rating agencies, Moody's and Standard & Poor's, with S&P--though not Moody's--placing Greenland on the edge of default.

Investors "shocked"

China State-Backed Builder Rocks Bond Market With Delay Plan, Bloomberg reported 5/26/22:

A Chinese property company long considered among the nation’s most resilient shocked investors with a proposed dollar-bond payment delay, raising fresh doubts about the financial strength of the industry’s higher-rated borrowers.

Greenland Holdings Corp., whose shareholders include the Shanghai government, is asking holders of a $488 million dollar note due June 25 to delay repayment by a year, a rare sign of stress at a state-linked firm. Its bond price tumbled from highs of 92 cents on the dollar to a record low of 41 cents in recent days...

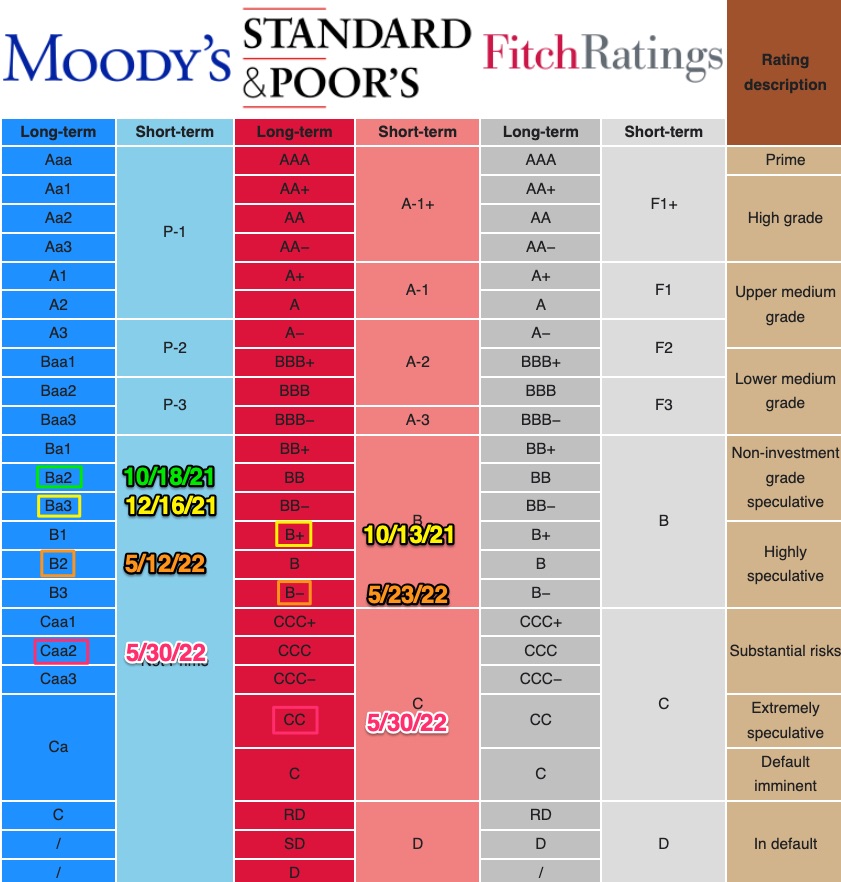

|

| Annotation of Wikipedia chart on bond rating categories |

The impact in Brooklyn?

The Real Deal got a boilerplate quote from a spokesperson representing the joint venture, dominated by Greenland USA, that's the master developer for Atlantic Yards/Pacific Park:

“Greenland Forest City Partners is fully committed to continuing to fulfill our obligations at Pacific Park Brooklyn, with incredible progress underway and major milestones upcoming,” said a spokesperson for Greenland Forest City Partners. “This summer we will commence work on the platform that will support the next phase of the project.”October 3, 2021, S&P: two-notch drop

"The review for downgrade reflects the uncertainty over the company's ability to generate enough operating cash flow to materially reduce its debt to more sustainable levels while maintaining ongoing access to funding and adequate liquidity, given the tight funding environment in the property sector," adds [Moody's Kaven] Tsang.Moody's noted the ownership:

Headquartered in Shanghai, Greenland Holding Group Company Limited is a state-controlled enterprise that primarily focuses on the real estate sector, with businesses in construction, finance and auto dealerships as well. The Shanghai SASAC [State-owned Assets Supervision and Administration Commission] indirectly owns 46.37% of Greenland Holding as of June 2021.

December 16, 2021, Moody's: one-notch drop

A 12/16/21 announcement from Moody's, Moody's downgrades ratings of Greenland Holdings and Greenland HK; outlook negative, indicated a one-notch drop to Ba3 from Ba2, with a negative outlook:

"The downgrades reflect our expectation that Greenland Holding's and Greenland Hong Kong's property sales will fall over the next 6-12 months because of tough business and funding conditions. Weakened operations will worsen the company's profitability and financial metrics," says Kaven Tsang, a Moody's Senior Vice President.

...Moody's expects Greenland Holding's liquidity to remain adequate over the next 12-18 months. Nevertheless, the company has sizable refinancing needs over the period. In particular, it has USD2.7 billion of US dollar bonds maturing between December 2021 and December 2022.May 12, 2022, Moody's: two-notch drop

A 5/12/22 announcement from Moody's, Moody's downgrades ratings of Greenland Holding and Greenland HK; places ratings on review for downgrade, indicated a two-notch drop to B2 from Ba3:

"The downgrade reflects our expectation that Greenland Holding's refinancing risk will increase over the next 6-12 months, driven by its declining contracted sales and operating cash flow, as well as sizable bond maturities," says Daniel Zhou, a Moody's Analyst.

...Meanwhile, Moody's estimates that a significant portion of the company's cash resides at the subsidiary or project levels under the property and construction segments, which could not be used to repay its debt at the holding company level.

The latter suggests that Greenland USA may be somewhat insulated, if it can raise the cash by selling more development rights in Brooklyn.

May 23, 2022, S&P: two-notch drop

A 5/23/22 announcement from S&P, Greenland Holding, Subsidiary Greenland Hong Kong Downgraded To 'B-' On Weak Liquidity; Ratings On CreditWatch Negative, indicated a two-notch drop to B- from B+:

Greenland Holding Group Co. Ltd.'s (Greenland) liquidity is deteriorating amid the industry downcycle. We have revised our assessment of the company's liquidity to weak from less than adequate due to its depleting accessible cash and declining sales...

With Greenland's limited funding channels, the company will need to heavily rely on cash flow from property sales, asset disposals, and refinancing of its onshore bank loans to meet its short-term debt maturities.

Greenland's cash generation from sales will weaken amid tough operating conditions.We believe an imminent recovery is unlikely, given the weak market sentiment and ongoing city lockdowns in China.

May 30, 2022, Moody's: three-notch drop

A 5/30/22 announcement from Moody's, Moody's downgrades ratings of Greenland Holding and Greenland HK; outlook negative, indicated a three-notch drop to Caa2 from B2:

"The downgrade reflects Greenland Holding's elevated liquidity risks, following its consent solicitation to extend the maturity of its offshore bond due in June 2022," says Daniel Zhou, a Moody's Analyst.

...The proposed maturity extension indicates Greenland Holding's escalating liquidity pressure due to difficult operating and funding conditions in China's property market and its sizable debt maturities.

While Moody's said an upgrade was unlikely, it could happen "if Greenland Holding improves its funding access and materially reduces its refinancing risks."

May 30, 2022, S&P: four-notch drop

A 5/30/22 announcement from S&P, Greenland Holding Downgraded To 'CC' On Distressed Maturity Extension; Outlook Negative, indicated a four-notch drop to CC from B-:

On May 27, 2022, China-based property developer Greenland Holding Group Co. Ltd. (Greenland) commenced an offer to extend the maturity of its outstanding U.S. dollar notes due June 25, 2022.Greenland, suggested S&P, has "limited accessible cash" and its ability to sell property "remains adversely affected by the prolonged lockdown in Shanghai." That said, as of today, the two-month lockdown has eased, reports the AP.

We view the proposed transaction as a distressed maturity extension. We believe the company is vulnerable to nonpayment of its senior notes upon maturity in the absence of the proposed transaction. Upon completion of the transaction, we will assess it as tantamount to a default.

So, could Greenland pull off a recovery? We can't rule it out. The end of the lockdown might change the outlook. Stay tuned.

Comments

Post a Comment