On 9/8/16, the centrist Brookings Institution posted a summary of its new report, with the provocative headline, Why the federal government should stop spending billions on private sports stadiums. It pointed out that the use of tax-exempt municipal bonds to fund venue construction constitutes a major federal subsidy, estimated as $431 million for the new Yankee Stadium.

The Barclays Center

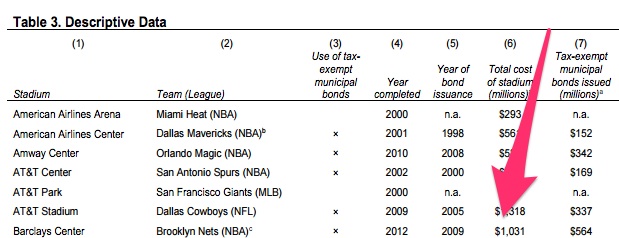

For the Barclays Center, now occupied by the Brooklyn Nets and New York Islanders, they estimate a federal subsidy of $122 million, with a total revenue loss of $161 million.

That's different from what the New York City Independent Budget Office estimated in 2009: $193.9 million, which was overstated by nearly 25%, so it should then have been $146.1 million.

Why do I say it was overstated? It was calculated based on an estimated $678 million in tax-exempt bonds, but $511 million were ultimately sold. (I'm not sure why Brookings says $564 million. Note: Brookings used $564 million because it was adjusted to 2014 dollars.) And it likely would be different if it were recalculated, given that the arena bonds were recently refinanced.

So why did Brookings choose $122 million rather than $146.1 million?Not sure, but I suspect there were different underlying assumptions about interest rates. Note the comment from Brookings:

That concept has been raised before, but the study points to an additional loss in federal tax revenues, a "windfall tax break" for bondholders, such as $61 million for Yankee Stadium. So that reaches $492 million.

The Barclays Center figure is $122 million and, thanks to that tax break, $161 million (though both totals deserve a caveat, as I explain below).

The Real Deal summarized it as Three NYC stadiums received $867M in federal subsidies: study. Those three venues--Yankee Stadium, Barclays Center, and CitiField--represented about one-quarter of the national total.

The report

In the full report, more soberly titled, “Tax-exempt municipal bonds and the financing of professional sports stadiums,” Brookings Senior Fellow Ted Gayer, Austin J. Drukker, and Alexander K. Gold quantify the federal subsidies to finance professional sports stadiums built or renovated since 2000, estimating a total of $3.2 billion federal taxpayer dollars, as of 2014, assuming a 3% discount rate.

The Barclays Center figure is $122 million and, thanks to that tax break, $161 million (though both totals deserve a caveat, as I explain below).

The Real Deal summarized it as Three NYC stadiums received $867M in federal subsidies: study. Those three venues--Yankee Stadium, Barclays Center, and CitiField--represented about one-quarter of the national total.

The report

In the full report, more soberly titled, “Tax-exempt municipal bonds and the financing of professional sports stadiums,” Brookings Senior Fellow Ted Gayer, Austin J. Drukker, and Alexander K. Gold quantify the federal subsidies to finance professional sports stadiums built or renovated since 2000, estimating a total of $3.2 billion federal taxpayer dollars, as of 2014, assuming a 3% discount rate.

But because high-income bond holders receive a windfall gain for holding municipal bonds, the resulting loss in total federal revenue rises to $3.7 billion.

The Barclays Center

For the Barclays Center, now occupied by the Brooklyn Nets and New York Islanders, they estimate a federal subsidy of $122 million, with a total revenue loss of $161 million.

That's different from what the New York City Independent Budget Office estimated in 2009: $193.9 million, which was overstated by nearly 25%, so it should then have been $146.1 million.

Why do I say it was overstated? It was calculated based on an estimated $678 million in tax-exempt bonds, but $511 million were ultimately sold. (

So why did Brookings choose $122 million rather than $146.1 million?

We use the interest rate spread between Moody's Aa-rated corporate and municipal bonds (which in 2009, the year of issuance, was 1.24 percentage points), and compute the present value of the subsidy for each bond listed in the official statement using equation 2 in our paper (and a discount rate of 3%).

Little or no benefits

The study says there is "little evidence that stadiums provide even local economic benefits" and "clearly no economic justification for federal subsidies for sports stadiums," since residents of a faraway state gain nothing from a relocation decision.

The Atlantic's CityLab summarized it as Should the Federal Government Be Funding Private Sports Stadiums?, quoting lead author Ted Gayer:

The study says there is "little evidence that stadiums provide even local economic benefits" and "clearly no economic justification for federal subsidies for sports stadiums," since residents of a faraway state gain nothing from a relocation decision.

That raises the question: "So why is the federal government still subsidizing their construction?" The report explains the history:

The authors suggest a reform:

Until the early 1950s, most professional sports stadiums were privately built. That changed in 1953 when the Boston Braves were lured to Milwaukee by a new stadium built with public money. Since then, public funding of stadiums has been the norm.What should be done?

In 1986, Congress tried to rein in this practice with the Tax Reform Act of 1986. But the reforms backfired, and instead encouraged state and local governments to offer generous financing packages in order for the financing to qualify for the federal subsidies.

The authors suggest a reform:

Congress to eliminate the “private payment test” for stadiums. By doing so, any stadium used primarily for “private business use” (that is, all professional sports stadiums) would no longer be eligible to receive federal tax-exempt financing.The coverage

An alternative approach would be to limit, rather than eliminate, the federal tax subsidy by mandating tax-exempt stadium bonds be deemed “qualified private activity bonds,” which are subject to a statewide volume cap.

The Atlantic's CityLab summarized it as Should the Federal Government Be Funding Private Sports Stadiums?, quoting lead author Ted Gayer:

A cross-state bridge or infrastructure project, Gayer says, should receive federal funds; in contrast, stadiums—which have spillover benefits for a much smaller locality—should be subsidized by the people they serve...The "solution to what CityLab has previously termed “the never-ending stadium boondoggle” is to treat them like corporate properties, not public goods," as the president has proposed.

The stoking of intense local fanaticism aside, stadiums offer few benefits even at the city level. “Proponents of government subsidies for sports stadiums typically justify them on the grounds that stadiums provide spillover gains to the local economy,” Gayer wrote in the Brookings report. But he added that “academic studies consistently find no discernible positive relationship between sports facility construction and local economic development, income growth, or job creation.” Even if one persists in believing stadiums offer spillover economic benefits, Gayer wrote, there’s no justification to keep throwing federal money at them.

In his Field of Schemes blog, Neil deMause wrote Tax-free stadium bonds cost U.S. taxpayers $3.7B since 2000 for no damn reason, says study, offering some history:

It’s been public knowledge for decades that the federal government spends billions of dollars subsidizing private sports stadiums through tax-free bonds for no good reason: Sen. Daniel Patrick Moynihan tried (and failed) to address it in 1986 through the Tax Reform Act and again ten years later, Congress has held hearings about it where myself and others testified, and President Obama has proposed eliminating the tax-exempt bond loophole in his annual budget.He's skeptical, though, of change:

Still, that’s not the same as a major think tank actually itemizing the cost....

Whether all this attention results in anything being done about the situation is another story: When Moynihan tried to pass a bill in the ’90s to rein in federal stadium subsidies, the New York Times reported that he’d been forced to “retreat under a hail of lobbying fire,” and matters aren’t likely to be much different today.…

From the report: national benefits?

The authors write:

Sports stadiums do not exhibit economies of scale, so there is no natural monopoly justification for government subsidies. Instead, the justification often given for government subsidies for such stadiums—particularly local subsidies—is that there are spillover gains to the local economy from a stadium that are greater than the cost of the subsidies to local taxpayers (Josza, 2003). The evidence for large spillover gains from stadiums to the local economy is weak. Academic studies consistently find no discernible positive relationship between sports facility construction and local economic development, income growth, or job creation (Baim, 1994; Rosentraub et al., 1994; Baade, 1996; Zimmerman, 1996; Noll and Zimbalist, 1997; Coates and Humphreys, 1999, 2008; Siegfried and Zimbalist, 2000; Josza, 2003). Indeed, after 20 years of academic research on the topic, “Articles published in peer reviewed economics journals contain almost no evidence that professional sports franchises and facilities have a measurable economic impact on the economy” (Coates and Humphreys, 2008, p. 302). And as Siegfried and Zimbalist (2000, p. 103) put it, “Few fields of empirical economic research offer virtual unanimity of findings … that there is no statistically significant positive correlation between sports facility construction and economic development.”

(Emphasis added)

Remember, Andrew Zimbalist's "study" for Atlantic Yards developer Forest City Ratner was never peer-reviewed, and deeply flawed.

From the report: local benefits?

What about local benefits? The authors write:

Remember, Andrew Zimbalist's "study" for Atlantic Yards developer Forest City Ratner was never peer-reviewed, and deeply flawed.

From the report: local benefits?

What about local benefits? The authors write:

Even if one believes, contrary to the empirical evidence, that the spillover benefits to the local economy justify taxpayer support, or that the benefits to local residents of following and talking about the home team are substantial, there still remains no economic justification for federal subsidies for sports stadiums. Residents of, say, Wyoming, Maine, or Alaska, gain nothing from the Washington-area football team’s decision to locate in Virginia, Maryland, or the District of Columbia. Yet, under current federal law, taxpayers throughout the country could ultimately subsidize the stadium, wherever it is located.

Maybe that's why Zimbalist's study addressed only the impact on New York City and State treasuries, and ignored the federal impact.

Looking at reforms

Looking at reforms

The authors write:

Eliminating the private payment test for stadium financing would mean that bonds to finance stadiums would be taxable private activity bonds if more than 10 percent of the facility is used for private business use, which undoubtedly would be the case. The Joint Committee on Taxation (2005) and the Obama administration’s previous two budgets (U.S. Department of Treasury, 2015, 2016) proposed this elimination of the private payment test for stadium financing in order to eliminate the federal subsidy.

Another approach would limit the subsidy, given a state cap on tax-exempt qualified private activity bonds

this policy change would have several effects, including forcing states to choose between federal tax subsidy for stadium financing versus for other qualified financing under the volume cap; allowing state and local governments to use taxes directed at the beneficiaries of the stadiums to finance the tax-exempt bonds; and eliminating the tax subsidy for stadium luxury boxes, since the law does not allow the proceeds from tax-exempt qualified private activity bonds to finance such things. Additionally, current law requires that such bonds be expressly approved by either a voter referendum or by an elected representative after a public hearing following reasonable notice to the public, which would increase the transparency of stadium deals that benefit from tax-exempt financing (Internal Revenue Service, 2016).

(Emphasis added)

The Barclays Center data

The Barclays Center data

The researchers gathered information on venue bonds from the Electronic Municipal Market Access website collected cost data websites including this Marquette site and these arena sites.

Great post, you clearly read the the whole paper thoroughly. To address just a few of your quibbles: We use $564 million for Barclays because that is $511 million 2009 dollars adjusted to 2014 dollars. Remember everything is adjusted to 2014 dollars. The official statement for the Barclays bonds can be found here: http://emma.msrb.org/SecurityView/SecurityDetails.aspx?cusip=A4F627B4594C1054F2E1CD71789D7AB46. We use the interest rate spread between Moody's Aa-rated corporate and municipal bonds (which in 2009, the year of issuance, was 1.24 percentage points), and compute the present value of the subsidy for each bond listed in the official statement using equation 2 in our paper (and a discount rate of 3%).

ReplyDelete