The strategy under which the Empire State Development Corporation (ESDC) and developer Forest City Ratner seek tax-exempt bonds for the Atlantic Yards arena has been acknowledged by the chief counsel of the Internal Revenue Service (IRS) as a “loophole” the agency moved quickly to eliminate.

Donald Korb’s testimony came at a 3/29/07 oversight hearing of the Domestic Policy Subcommittee of the House Committee on Oversight and Reform, headed by Rep. Dennis Kucinich (D-OH). The hearing, covering “Taxpayer Financed Stadiums, Convention Centers, and Hotels,” mainly focused on the stadiums, starting from the premise that they do not bring economic development and potentially divert funds from critical infrastructure.

Donald Korb’s testimony came at a 3/29/07 oversight hearing of the Domestic Policy Subcommittee of the House Committee on Oversight and Reform, headed by Rep. Dennis Kucinich (D-OH). The hearing, covering “Taxpayer Financed Stadiums, Convention Centers, and Hotels,” mainly focused on the stadiums, starting from the premise that they do not bring economic development and potentially divert funds from critical infrastructure.

The IRS in July 2006 issued two Private Letter Rulings (PLRs) related to financing for stadiums for the New York Yankees and the New York Mets. (Here's one.) In both cases, the IRS agreed that payments in lieu of taxes (PILOTs) used to pay off the bonds could substitute for property taxes, even though critics warn that they do not seem commensurate with such taxes but simply mirror debt service.

The use of PILOTs, paid for by the team owners, saves the local governments from legal restrictions that otherwise would require tax-exempt bonds for stadiums to be repaid by governmental sources of funds, including generally applicable taxes, like sales taxes or hotel taxes.

Notably, the PILOT payments were set at a fixed amount by agreement between the teams and the ESDC. While that number could easily be tied to annual bond repayments, taxes often fluctuate. And bond buyers, as Neil deMause explains on his Field of Schemes blog, don't like uncertainty in their bond payments.

Under the proposed change by the IRS, according to testimony (PDF) by Korb, “[E]ligible PILOT payments must be based on the current assessed value of the property for property taxes for each year in which the PILOTs are paid, and the assessed value must be determined in the same manner and with the same frequency as property subject to generally applicable taxes. A payment is not commensurate if it is based in any way on debt service on an issue or is otherwise set at a fixed dollar amount that cannot vary with the assessed value of the property.”

Under the proposed change by the IRS, according to testimony (PDF) by Korb, “[E]ligible PILOT payments must be based on the current assessed value of the property for property taxes for each year in which the PILOTs are paid, and the assessed value must be determined in the same manner and with the same frequency as property subject to generally applicable taxes. A payment is not commensurate if it is based in any way on debt service on an issue or is otherwise set at a fixed dollar amount that cannot vary with the assessed value of the property.”

Tax exempt bonds save developers money because those buying the bonds accept a lower interest rate--on $800 million worth of Atlantic Yards arena bonds, I estimated that Forest City Ratner might save $165 million. Federal taxpayers, not state or city ones, bear the brunt of the burden.

NY strikes back

In a May 8 letter to the U.S. Treasury Department and the IRS, according to an article last Friday in The Bond Buyer, officials from the New York City Industrial Development Agency and the ESDC have argued that the proposed regulations, which would apply to bonds sold after 2/18/07, should not apply to the Yankees or Mets, both of which expect to sell additional PILOT bonds within the year, or to the Atlantic Yards arena.

"The impact of the proposed effective date is that projects that were in progress long before the proposed regulations were issued are prevented from going forward," according to the letter. "This broad impact did not seem intended" by the proposed regulations.

The letter asked for the rules to be suspended until 2/19/09, with an exception for the Atlantic Yards project in case litigation further delays bond sales. However, the letter suggested that the first PILOT bonds for the Atlantic Yards arena would be be issued by the ESDC this year--which is questionable, since litigation may linger.

Meanwhile, in a letter sent May 23, Kucinich asked the IRS and Treasury Department to desist from approving any more sports facility deals based on PILOTs, pending further clarification of their policies. He was essentially questioning whether the IRS should have granted the PLRs in the first place. The IRS regulations were actually scheduled to go into effect in early 2007, but apparently have been postponed.

(The May 8 letter is apparently what has triggered the recent news coverage about the issue.)

From the GPP

From the GPP

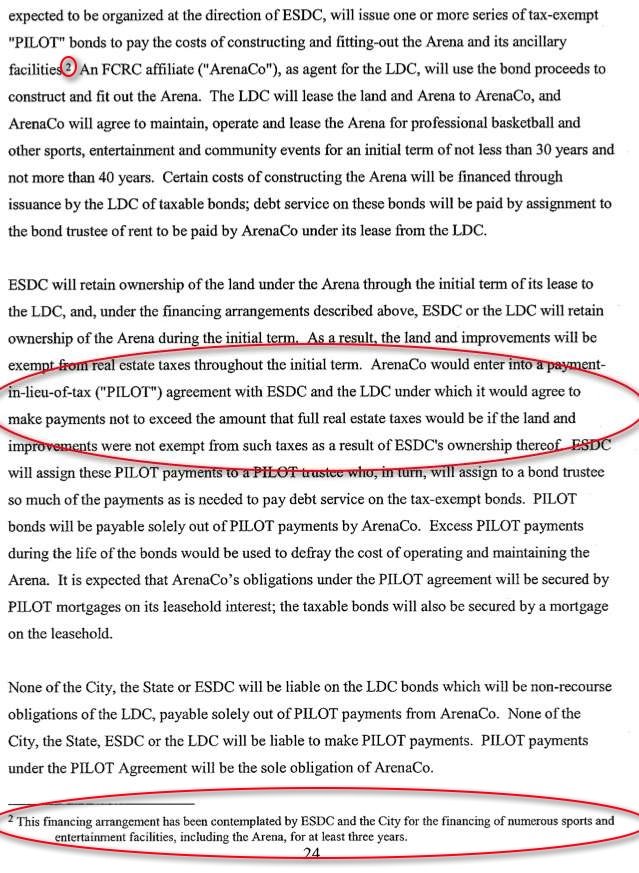

From page 24 of the Atlantic Yards General Project Plan or GPP (Part 2), approved 12/8/06:

ArenaCo would enter into a payment-in-lieu-of-tax ("PILOT") agreement with ESDC and the LDC under which it would agree to make payments not to exceed the amount that full real estate taxes would be if the land and improvements were not exempt from such taxes as a result of ESDC's ownership thereof.

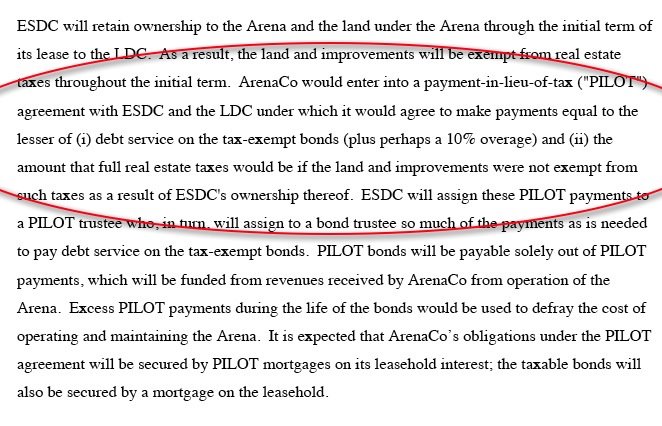

Note that the footnote indicates that the financing has been "contemplated" by the ESDC and the city "for at least three years," but it doesn't say that the process has been legitimized. An earlier version of the General Project Plan, issued 7/18/06 (below) indicates that the payments might be equal to debt service rather than property taxes.

indicates that the payments might be equal to debt service rather than property taxes.

From Field of Schemes

Author deMause’s book Field of Schemes (written with Joanna Cagan), describes the Yankees and Mets deals (p. 311):

The other remaining obstacle affected both teams and involved the $1.56 billion in tax-exempt bonds that would be used to raise money for construction. Ever since the 1986 Tax Reform Act, it had been considered illegal to use federally subsidized bonds for projects where more than 10 percent of the cost would be repaid by a private entity. The Mets and Yankees stadiums were to use 100 percent private money to repay the bonds--but, the city claimed, these payments were technically not private but rather "in lieu of" the property taxes that the teams were not going to have to pay.

It was a distinction fine enough to raise more than a few eyebrows among development experts. One national bond expert, speaking on condition of anonymity, called the city's argument "a transparent end run around the 1986 provision saying stadiums cannot be financed with private-activity bonds. We have simply interposed an empty box into which the Yankees' stadium-related revenue would be placed, labeled that box 'PILOT,' and transformed black into white. If only solving the problems of real life were that simple."

It was a distinction fine enough to raise more than a few eyebrows among development experts. One national bond expert, speaking on condition of anonymity, called the city's argument "a transparent end run around the 1986 provision saying stadiums cannot be financed with private-activity bonds. We have simply interposed an empty box into which the Yankees' stadium-related revenue would be placed, labeled that box 'PILOT,' and transformed black into white. If only solving the problems of real life were that simple."

Dan Steinberg [of the watchdog group Good Jobs New York] recalls a meeting of the city council's finance committee where members split unprecedented semantic hairs over the difference between "public" and "private" money. "The entire point of the hearing was to determine whether or not the council was comfortable using money that the city would normally collect," he says. "But meanwhile, throughout this very hearing, you had council members defending the project by arguing that it was privately financed. I remember thinking, if the IRS were in this room, and heard the arguments that the council members were making, it would be very difficult to justify the use of payments in lieu of taxes."

No public purpose?

During the 3/29/07 hearing, Kucinich questioned Dennis Zimmerman, Director of Projects at the American Tax Policy Institute and, as deMause now says, the “national bond expert” quoted in his book. (The institute is a nonpartisan organization; Zimmerman was speaking personally. The quotes come from watching a C-SPAN video of the hearing.)

During the 3/29/07 hearing, Kucinich questioned Dennis Zimmerman, Director of Projects at the American Tax Policy Institute and, as deMause now says, the “national bond expert” quoted in his book. (The institute is a nonpartisan organization; Zimmerman was speaking personally. The quotes come from watching a C-SPAN video of the hearing.)

DK: "You are a former Congressional Research Service and Congressional Budget Office analyst. In your opinion, what is the public purpose fulfilled by tax-exempt financing of the construction of Yankee Stadium?"

Zimmerman allowed himself a small smile.

DZ: "If you go by the structure of the bond rules prior to the [ruling], it would not have been allowed. In general, since these things provide no benefit to federal taxpayers, it’s not clear why one would want to subsidize these things."

DK: "Has the IRS, in its rulings for the Yankees and the Mets, adhered to the meaning and the intent of the law?"

DZ: "The meaning and intent of the law is sort of in the eye of the beholder, frequently. As I read the law, prior to the PILOT ruling, it is not consistent."

DK: "How would you characterize the impact of the IRS rulemaking on the 1986 law?"

DZ: "It circumvents what the 1986 Tax Act rules say, because it reclassifies stadium-related revenue, which clearly should be counted against the 10% security interest test, it reclassified it as generally applicable taxes, and converted these things from private activity bonds, which are taxable, into governmental bonds, which are tax-exempt."

Rep. John Tierney (D-MA) asked Zimmerman to explain the rules.

Rep. John Tierney (D-MA) asked Zimmerman to explain the rules.

DZ: "Bonds are taxable or tax-exempt depending upon two tests. One is whether more than more than 10% of the bond proceeds are used by a private business. The second is whether more than 10% of the debt service is secured by property used in a trade or business. You have to exceed the 10% for both of those. So, for a stadium, obviously more than 10% of bond proceeds are being used by a private entity. So the question... is: can you structure the deal that no more than 10% of the debt service is paid for by stadium-related revenue, that’s the property being used in the trade or business. The ‘86 act said, if you don’t satisfy that 10% security interest test, you can’t issue a stadium bond. So it would have to be a governmental bond, which forces you to finance it with general tax revenues."

JT: "So the IRS rulemaking letter--was that an interpretation or a change in law?"

DZ: I’m not a lawyer. I can only tell you what the effect was. It converted what, absent the PILOTs ruling, would’ve been considered stadium-related revenue, and would have classified it as a taxable private-activity bond. It would not have been eligible for tax-exempt financing."

The IRS testimony

Korb, in his testimony, acknowledged that “[d]ifficult interpretative issues arise when a payment purporting to be a generally applicable tax is imposed in a customized fashion on a private business that uses bond-financed property... This line becomes particularly difficult to draw when the tax is abated through negotiations or is a PILOT that is specifically crafted for the transaction and essentially results in debt service being fully paid by the private business.”

The plan for PILOT payments set at a fixed amount for the New York stadium deals generated “serious concerns” at the IRS, but, Korb testified, 1997 regulations issued by the Treasury Department under the Clinton administration “compelled the result.”

However, IRS then concluded that existing regulations “could be interpreted to permit PILOTs to be used to pay debt service on tax-exempt bonds in situations where the PILOTs bear an insufficient link to the otherwise generally applicable tax, and in fact closely resemble the expected debt service on the bonds.”

Hence the proposed regulations. “We spotted a flaw in the 1997 Treasury regulations, and we moved expeditiously to fix it,” Korb said.

(I haven't yet found a link to those regulations.)

Korb under the gun

During the hearing Kucinich questioned Korb as to whether the Yankees should have been concerned the plan wouldn’t be allowed. He wouldn’t acknowledge that, but did acknowledge that the Yankees would have had to choose a very different strategy. “ That’s why we moved very very quickly to eliminate the loophole created in 1997,” he said.

While Kucinich queried Korb about whether the PLR would let the Yankees owner keep a greater share of the revenues and whether the new stadium would raise the value of the team, the lawyer begged off, saying he was a tax lawyer, not a sports lawyer.

Kucinich asked Korb if he agreed with Zimmerman’s testimony that the interpretation violates the 1986 tax act. Korb said no, that it was based on the 1997 interpretation. “We felt our hands were tied,” he said.

Kucinich still skeptical

Kucinich remained skeptical, noting that the PLRs rely on the stated purpose that the payments are for “economic development and recreational opportunities in the City” that would be generated by using the PILOTs to pay for the bonds:. “As you’ve heard, there’s a consensus among economists that stadium construction does not lead to economic growth. Did the IRS simply accept at face value the claims of stadium financing applicants... or did you try to verify the representations?”

Korb said the IRS had no discretion.

Kucinich’s letter

In his May 23 letter to IRS and Treasury, Kucinich returned to the issue, writing, "In the PLRs, the Treasury Department uncritically accepted the position of the proponents of the Yankees' and Mets' deals that the PILOTs were 'designated for a public purpose' because they would 'promote and encourage economic development opportunities in City.'”

A bond attorney quoted in the newspaper said local officials are not responsible for determining if stadiums are a public good.

Kucinich also accused Eric Solomon, a Treasury Department official, of offering a misleading response regarding the department’s discretion to regulate PILOTs rather than wait for Congress to act.

Zimmerman testimony

In his testimony (PDF), Zimmerman explained that the Tax Reform Act of 1986 made stadiums ineligible for private-activity bonds, previously known as industrial development bonds. As he testified, "The expectation was that local governments would be reluctant to use the other option, governmental debt, to finance stadiums, and the use of tax-exempt debt for financing stadiums would wither."

However, Zimmerman said, "those who benefit most from stadiums (owners of teams, players, fans, some related businesses) learned how to utilize pseudo-economic studies to argue that the economic benefits from stadiums generated sufficient additional tax revenue to pay for the public subsidy, a proposition that runs counter to an extensive economics literature.... Second, the monopolistic structure of professional sports leagues maintains excess demand for franchises, forcing cities to compete for a limited number of franchises with offerings of stadium subsidies. As a result, many stadiums were built for which local taxpayers, who receive limited benefits, paid at least 90 percent of the debt service on the bonds."

“Creative” PLRs

In 2006, the IRS approved what Zimmerman called a "creative" effort when it agreed, via the PLRs, that "stadium-related revenue could be used to pay the debt service on governmental debt. Since 1986, payment of more than 10 percent of debt service with stadium-related revenue would make the bonds taxable private-activity bonds. But IRS ruled that stadium-related revenue is actually payments in lieu of taxes (PILOTs) and qualifies as generally applicable taxes, not as revenue arising from private business activity."

He warned that the PILOT ruling, while attractive to local taxpayers and better than using general tax revenues for stadium financing, increases federal subsidies of stadiums and “might open the door for widespread tax-exempt governmental bond financing of private investment projects” and “raises the prospect of making elected officials into commercial bankers in charge of allocating ever-larger portions of the nation’s scarce supply of savings.”

He recommended a compromise: "[A]d stadiums to the list of private activities eligible for tax-exempt financing; subject stadium bonds to the private-activity bond volume cap; and wipe the PILOT precedent off the books. Private-activity bond financing would encourage use of the benefit principle of taxation. Requiring stadium projects to compete for scarce private-activity bond volume cap with other eligible private activities such as mortgage revenue bonds, small-issue industrial development bonds, and student loan bonds would minimize the federal subsidy. And eliminating the PILOT precedent would prevent its indiscriminate application to a broad range of private activities and would control elected officials’ role of commercial bankers."

The "volume cap" means that only a limited amount of bonds can be issued, as opposed to the unlimited amount of bonds under the current plan.

Donald Korb’s testimony came at a 3/29/07 oversight hearing of the Domestic Policy Subcommittee of the House Committee on Oversight and Reform, headed by Rep. Dennis Kucinich (D-OH). The hearing, covering “Taxpayer Financed Stadiums, Convention Centers, and Hotels,” mainly focused on the stadiums, starting from the premise that they do not bring economic development and potentially divert funds from critical infrastructure.

Donald Korb’s testimony came at a 3/29/07 oversight hearing of the Domestic Policy Subcommittee of the House Committee on Oversight and Reform, headed by Rep. Dennis Kucinich (D-OH). The hearing, covering “Taxpayer Financed Stadiums, Convention Centers, and Hotels,” mainly focused on the stadiums, starting from the premise that they do not bring economic development and potentially divert funds from critical infrastructure.The IRS in July 2006 issued two Private Letter Rulings (PLRs) related to financing for stadiums for the New York Yankees and the New York Mets. (Here's one.) In both cases, the IRS agreed that payments in lieu of taxes (PILOTs) used to pay off the bonds could substitute for property taxes, even though critics warn that they do not seem commensurate with such taxes but simply mirror debt service.

The use of PILOTs, paid for by the team owners, saves the local governments from legal restrictions that otherwise would require tax-exempt bonds for stadiums to be repaid by governmental sources of funds, including generally applicable taxes, like sales taxes or hotel taxes.

Notably, the PILOT payments were set at a fixed amount by agreement between the teams and the ESDC. While that number could easily be tied to annual bond repayments, taxes often fluctuate. And bond buyers, as Neil deMause explains on his Field of Schemes blog, don't like uncertainty in their bond payments.

Under the proposed change by the IRS, according to testimony (PDF) by Korb, “[E]ligible PILOT payments must be based on the current assessed value of the property for property taxes for each year in which the PILOTs are paid, and the assessed value must be determined in the same manner and with the same frequency as property subject to generally applicable taxes. A payment is not commensurate if it is based in any way on debt service on an issue or is otherwise set at a fixed dollar amount that cannot vary with the assessed value of the property.”

Under the proposed change by the IRS, according to testimony (PDF) by Korb, “[E]ligible PILOT payments must be based on the current assessed value of the property for property taxes for each year in which the PILOTs are paid, and the assessed value must be determined in the same manner and with the same frequency as property subject to generally applicable taxes. A payment is not commensurate if it is based in any way on debt service on an issue or is otherwise set at a fixed dollar amount that cannot vary with the assessed value of the property.”Tax exempt bonds save developers money because those buying the bonds accept a lower interest rate--on $800 million worth of Atlantic Yards arena bonds, I estimated that Forest City Ratner might save $165 million. Federal taxpayers, not state or city ones, bear the brunt of the burden.

NY strikes back

In a May 8 letter to the U.S. Treasury Department and the IRS, according to an article last Friday in The Bond Buyer, officials from the New York City Industrial Development Agency and the ESDC have argued that the proposed regulations, which would apply to bonds sold after 2/18/07, should not apply to the Yankees or Mets, both of which expect to sell additional PILOT bonds within the year, or to the Atlantic Yards arena.

"The impact of the proposed effective date is that projects that were in progress long before the proposed regulations were issued are prevented from going forward," according to the letter. "This broad impact did not seem intended" by the proposed regulations.

The letter asked for the rules to be suspended until 2/19/09, with an exception for the Atlantic Yards project in case litigation further delays bond sales. However, the letter suggested that the first PILOT bonds for the Atlantic Yards arena would be be issued by the ESDC this year--which is questionable, since litigation may linger.

Meanwhile, in a letter sent May 23, Kucinich asked the IRS and Treasury Department to desist from approving any more sports facility deals based on PILOTs, pending further clarification of their policies. He was essentially questioning whether the IRS should have granted the PLRs in the first place. The IRS regulations were actually scheduled to go into effect in early 2007, but apparently have been postponed.

(The May 8 letter is apparently what has triggered the recent news coverage about the issue.)

From the GPP

From the GPPFrom page 24 of the Atlantic Yards General Project Plan or GPP (Part 2), approved 12/8/06:

ArenaCo would enter into a payment-in-lieu-of-tax ("PILOT") agreement with ESDC and the LDC under which it would agree to make payments not to exceed the amount that full real estate taxes would be if the land and improvements were not exempt from such taxes as a result of ESDC's ownership thereof.

Note that the footnote indicates that the financing has been "contemplated" by the ESDC and the city "for at least three years," but it doesn't say that the process has been legitimized. An earlier version of the General Project Plan, issued 7/18/06 (below)

indicates that the payments might be equal to debt service rather than property taxes.

indicates that the payments might be equal to debt service rather than property taxes.From Field of Schemes

Author deMause’s book Field of Schemes (written with Joanna Cagan), describes the Yankees and Mets deals (p. 311):

The other remaining obstacle affected both teams and involved the $1.56 billion in tax-exempt bonds that would be used to raise money for construction. Ever since the 1986 Tax Reform Act, it had been considered illegal to use federally subsidized bonds for projects where more than 10 percent of the cost would be repaid by a private entity. The Mets and Yankees stadiums were to use 100 percent private money to repay the bonds--but, the city claimed, these payments were technically not private but rather "in lieu of" the property taxes that the teams were not going to have to pay.

It was a distinction fine enough to raise more than a few eyebrows among development experts. One national bond expert, speaking on condition of anonymity, called the city's argument "a transparent end run around the 1986 provision saying stadiums cannot be financed with private-activity bonds. We have simply interposed an empty box into which the Yankees' stadium-related revenue would be placed, labeled that box 'PILOT,' and transformed black into white. If only solving the problems of real life were that simple."

It was a distinction fine enough to raise more than a few eyebrows among development experts. One national bond expert, speaking on condition of anonymity, called the city's argument "a transparent end run around the 1986 provision saying stadiums cannot be financed with private-activity bonds. We have simply interposed an empty box into which the Yankees' stadium-related revenue would be placed, labeled that box 'PILOT,' and transformed black into white. If only solving the problems of real life were that simple."Dan Steinberg [of the watchdog group Good Jobs New York] recalls a meeting of the city council's finance committee where members split unprecedented semantic hairs over the difference between "public" and "private" money. "The entire point of the hearing was to determine whether or not the council was comfortable using money that the city would normally collect," he says. "But meanwhile, throughout this very hearing, you had council members defending the project by arguing that it was privately financed. I remember thinking, if the IRS were in this room, and heard the arguments that the council members were making, it would be very difficult to justify the use of payments in lieu of taxes."

No public purpose?

During the 3/29/07 hearing, Kucinich questioned Dennis Zimmerman, Director of Projects at the American Tax Policy Institute and, as deMause now says, the “national bond expert” quoted in his book. (The institute is a nonpartisan organization; Zimmerman was speaking personally. The quotes come from watching a C-SPAN video of the hearing.)

During the 3/29/07 hearing, Kucinich questioned Dennis Zimmerman, Director of Projects at the American Tax Policy Institute and, as deMause now says, the “national bond expert” quoted in his book. (The institute is a nonpartisan organization; Zimmerman was speaking personally. The quotes come from watching a C-SPAN video of the hearing.)DK: "You are a former Congressional Research Service and Congressional Budget Office analyst. In your opinion, what is the public purpose fulfilled by tax-exempt financing of the construction of Yankee Stadium?"

Zimmerman allowed himself a small smile.

DZ: "If you go by the structure of the bond rules prior to the [ruling], it would not have been allowed. In general, since these things provide no benefit to federal taxpayers, it’s not clear why one would want to subsidize these things."

DK: "Has the IRS, in its rulings for the Yankees and the Mets, adhered to the meaning and the intent of the law?"

DZ: "The meaning and intent of the law is sort of in the eye of the beholder, frequently. As I read the law, prior to the PILOT ruling, it is not consistent."

DK: "How would you characterize the impact of the IRS rulemaking on the 1986 law?"

DZ: "It circumvents what the 1986 Tax Act rules say, because it reclassifies stadium-related revenue, which clearly should be counted against the 10% security interest test, it reclassified it as generally applicable taxes, and converted these things from private activity bonds, which are taxable, into governmental bonds, which are tax-exempt."

Rep. John Tierney (D-MA) asked Zimmerman to explain the rules.

Rep. John Tierney (D-MA) asked Zimmerman to explain the rules.DZ: "Bonds are taxable or tax-exempt depending upon two tests. One is whether more than more than 10% of the bond proceeds are used by a private business. The second is whether more than 10% of the debt service is secured by property used in a trade or business. You have to exceed the 10% for both of those. So, for a stadium, obviously more than 10% of bond proceeds are being used by a private entity. So the question... is: can you structure the deal that no more than 10% of the debt service is paid for by stadium-related revenue, that’s the property being used in the trade or business. The ‘86 act said, if you don’t satisfy that 10% security interest test, you can’t issue a stadium bond. So it would have to be a governmental bond, which forces you to finance it with general tax revenues."

JT: "So the IRS rulemaking letter--was that an interpretation or a change in law?"

DZ: I’m not a lawyer. I can only tell you what the effect was. It converted what, absent the PILOTs ruling, would’ve been considered stadium-related revenue, and would have classified it as a taxable private-activity bond. It would not have been eligible for tax-exempt financing."

The IRS testimony

Korb, in his testimony, acknowledged that “[d]ifficult interpretative issues arise when a payment purporting to be a generally applicable tax is imposed in a customized fashion on a private business that uses bond-financed property... This line becomes particularly difficult to draw when the tax is abated through negotiations or is a PILOT that is specifically crafted for the transaction and essentially results in debt service being fully paid by the private business.”

The plan for PILOT payments set at a fixed amount for the New York stadium deals generated “serious concerns” at the IRS, but, Korb testified, 1997 regulations issued by the Treasury Department under the Clinton administration “compelled the result.”

However, IRS then concluded that existing regulations “could be interpreted to permit PILOTs to be used to pay debt service on tax-exempt bonds in situations where the PILOTs bear an insufficient link to the otherwise generally applicable tax, and in fact closely resemble the expected debt service on the bonds.”

Hence the proposed regulations. “We spotted a flaw in the 1997 Treasury regulations, and we moved expeditiously to fix it,” Korb said.

(I haven't yet found a link to those regulations.)

Korb under the gun

During the hearing Kucinich questioned Korb as to whether the Yankees should have been concerned the plan wouldn’t be allowed. He wouldn’t acknowledge that, but did acknowledge that the Yankees would have had to choose a very different strategy. “ That’s why we moved very very quickly to eliminate the loophole created in 1997,” he said.

While Kucinich queried Korb about whether the PLR would let the Yankees owner keep a greater share of the revenues and whether the new stadium would raise the value of the team, the lawyer begged off, saying he was a tax lawyer, not a sports lawyer.

Kucinich asked Korb if he agreed with Zimmerman’s testimony that the interpretation violates the 1986 tax act. Korb said no, that it was based on the 1997 interpretation. “We felt our hands were tied,” he said.

Kucinich still skeptical

Kucinich remained skeptical, noting that the PLRs rely on the stated purpose that the payments are for “economic development and recreational opportunities in the City” that would be generated by using the PILOTs to pay for the bonds:. “As you’ve heard, there’s a consensus among economists that stadium construction does not lead to economic growth. Did the IRS simply accept at face value the claims of stadium financing applicants... or did you try to verify the representations?”

Korb said the IRS had no discretion.

Kucinich’s letter

In his May 23 letter to IRS and Treasury, Kucinich returned to the issue, writing, "In the PLRs, the Treasury Department uncritically accepted the position of the proponents of the Yankees' and Mets' deals that the PILOTs were 'designated for a public purpose' because they would 'promote and encourage economic development opportunities in City.'”

A bond attorney quoted in the newspaper said local officials are not responsible for determining if stadiums are a public good.

Kucinich also accused Eric Solomon, a Treasury Department official, of offering a misleading response regarding the department’s discretion to regulate PILOTs rather than wait for Congress to act.

Zimmerman testimony

In his testimony (PDF), Zimmerman explained that the Tax Reform Act of 1986 made stadiums ineligible for private-activity bonds, previously known as industrial development bonds. As he testified, "The expectation was that local governments would be reluctant to use the other option, governmental debt, to finance stadiums, and the use of tax-exempt debt for financing stadiums would wither."

However, Zimmerman said, "those who benefit most from stadiums (owners of teams, players, fans, some related businesses) learned how to utilize pseudo-economic studies to argue that the economic benefits from stadiums generated sufficient additional tax revenue to pay for the public subsidy, a proposition that runs counter to an extensive economics literature.... Second, the monopolistic structure of professional sports leagues maintains excess demand for franchises, forcing cities to compete for a limited number of franchises with offerings of stadium subsidies. As a result, many stadiums were built for which local taxpayers, who receive limited benefits, paid at least 90 percent of the debt service on the bonds."

“Creative” PLRs

In 2006, the IRS approved what Zimmerman called a "creative" effort when it agreed, via the PLRs, that "stadium-related revenue could be used to pay the debt service on governmental debt. Since 1986, payment of more than 10 percent of debt service with stadium-related revenue would make the bonds taxable private-activity bonds. But IRS ruled that stadium-related revenue is actually payments in lieu of taxes (PILOTs) and qualifies as generally applicable taxes, not as revenue arising from private business activity."

He warned that the PILOT ruling, while attractive to local taxpayers and better than using general tax revenues for stadium financing, increases federal subsidies of stadiums and “might open the door for widespread tax-exempt governmental bond financing of private investment projects” and “raises the prospect of making elected officials into commercial bankers in charge of allocating ever-larger portions of the nation’s scarce supply of savings.”

He recommended a compromise: "[A]d stadiums to the list of private activities eligible for tax-exempt financing; subject stadium bonds to the private-activity bond volume cap; and wipe the PILOT precedent off the books. Private-activity bond financing would encourage use of the benefit principle of taxation. Requiring stadium projects to compete for scarce private-activity bond volume cap with other eligible private activities such as mortgage revenue bonds, small-issue industrial development bonds, and student loan bonds would minimize the federal subsidy. And eliminating the PILOT precedent would prevent its indiscriminate application to a broad range of private activities and would control elected officials’ role of commercial bankers."

The "volume cap" means that only a limited amount of bonds can be issued, as opposed to the unlimited amount of bonds under the current plan.

Just look how so many things happening right now come together: IRS loopholes, Atlantic Yards Reform legislation, the pursuit of subsidy and accountability to the community!

ReplyDeleteI was at the press conference today for the Atlantic Yards Governance Act bill being supported by Assembly members Hakeem Jeffries and Jim Brennan, and City Council members Letitia James and David Yassky as well as the Municipal Art Society and Brooklyn Heights Association. “The Campaign to Reform the Governance of Atlantic Yards.” (See the AYR post announcing the event was going to occur: http://atlanticyardsreport.blogspot.com/2008/06/ay-governance-bill-emerges-aimed-at.html) The bill could hold some promise.

The watchword phrase of the press conference was that the legislation is desperately needed so that there can be “accountability to the community.”

Accountability to the community cannot be achieved unless the public and its officials have real negotiating power when dealing with Forest City Ratner. There can be no negotiating power if Ratner is allowed to negotiate from the position of having a theoretical monopoly on development around Vanderbilt Yards. ESDC’s premise that its OK to award Ratner a theoretical monopoly on the development of 22 acres first and“negotiate” later the subsidy was always cockeyed and unworkable. The order has to be in reverse. No one should doubt this given Ratner’s recent bullying threats to leave the public with a Ratnerland-wasteland unless the public antes up more subsidy: Remember, the total amount of subsidy is, even now, something he leaves unspecified.

Now, as reported here, the same ESDC that came up with the bass-ackwards idea of developer-monopoly first, subsidy-negotiation second is in Washington D.C. lobbying for a tax code loophole so that private stadiums and arenas can be financed with tax-exempt bonds Perfect! because it has already been pointed out (by all sorts of people like David Cay Johnston) that this ineptly conceived subsidy cannot be effectively negotiated downward by municipalities for almost exactly the same reason: because the major sports franchises with which municipalities must negotiate operate as monopolies exempted from the laws of economic competition. Essentially, we have the embarrassment of ESDC as part of our New York delegation off in D.C. lobbying for public officials everywhere to have less negotiating power with the big developers and billionaires who own sports franchises. It doesn’t seem to matter to our ESDC people that the loophole they are lobbying for actually encourages the nonpayment of property taxes to the public. In the case of Atlantic Yards and Ratner’s Nets it is proposed that Ratner would be getting over $1.3 billion in taxpayer dollars paid to him by the time the arena was built. This is public accountability ESDC style!

Of course, in reality, in order for Ratner to actually have an actual monopoly at the Vanderbilt Yards development site Atlantic Yards would really have to be an “approved project” which it is not. At the press conference today there was discussion about whether anyone (other than Ratner) might consider “Atlantic Yards” an approved project. It simply isn’t. First, all sorts of subsidy and financing for the project has never been approved. Second, even if IRS and other hurdles are surmounted and subsidies were approved to proceed with the project as originally misconceived, it would still be necessary to go back to Public Authorities Control Board because Atlantic Yards with all its inflated costs is no longer the project they once acted on. But it doesn’t appear that the project is ever going to happen as it was originally misconceived. It is going to be a different project. And that project has not been approved.

Whatever happens, people were correct today when they said that legislation is needed to take this project away from ESDC so that accountability to the public can be achieved. And, just as true, Ratner’s theoretical monopoly on the project also needs to be taken away from him so that accountability to the public can be achieved.

Once we have accountability to the community and the public we can then proceed to have principled development- What would that mean? Among other things it most certainly includes, as one of its starting points, eliminating the unnecessary avenue and street closings as the Municipal Art Society has long been calling for. There would be proper processes without shortcuts circumventing community involvement and ULURP: For instance, this very importantly applies to upzoning and proposed condemnations. Also, see the 7 enumerated points at that Brooklyn Speaks site at: “Effective Action Needed From Brooklyn Speaks, BHA, etc. - MDDWhite | Mon, 03/17/2008 - 9:10am” http://www.brooklynspeaks.net/node/17#comment-1826

Michael D. D. White

Noticing New York